LLC vs Sole Proprietor for Freelancers: What Changes, What Does Not, and What It Costs

Somewhere around your first good freelance year, someone tells you that you need an LLC. A client asks for your business name on a W-9, or a freelancer friend mentions theirs, or a formation-service ad finds you, and suddenly staying a sole proprietor feels like walking around uninsured.

The pages ranking for this question do not help you think clearly about it. We fetched the top results in July 2026. A major marketplace's guide calls an LLC a "limited liability corporation" (it is a company, not a corporation) and tells you to file "articles of incorporation" to create one (the document is articles of organization). A big-brand advisor page answers "what does it cost" with "it depends on your state" and then presents three formation-service affiliate widgets. The strongest page on tax substance still never mentions that California charges $800 a year forever or that New York makes you buy six weeks of newspaper ads. Nobody compares the LLC against the boring alternative that actually covers a freelancer's biggest risk, which is professional liability insurance.

So here is the checked version, every number verified against the IRS, state filing offices, and primary sources this month. The short answer up front: the LLC decision is not a tax decision. One caveat too: this is general information, not legal or tax advice, and a CPA or business attorney who can see your specifics beats any article.

The short answer#

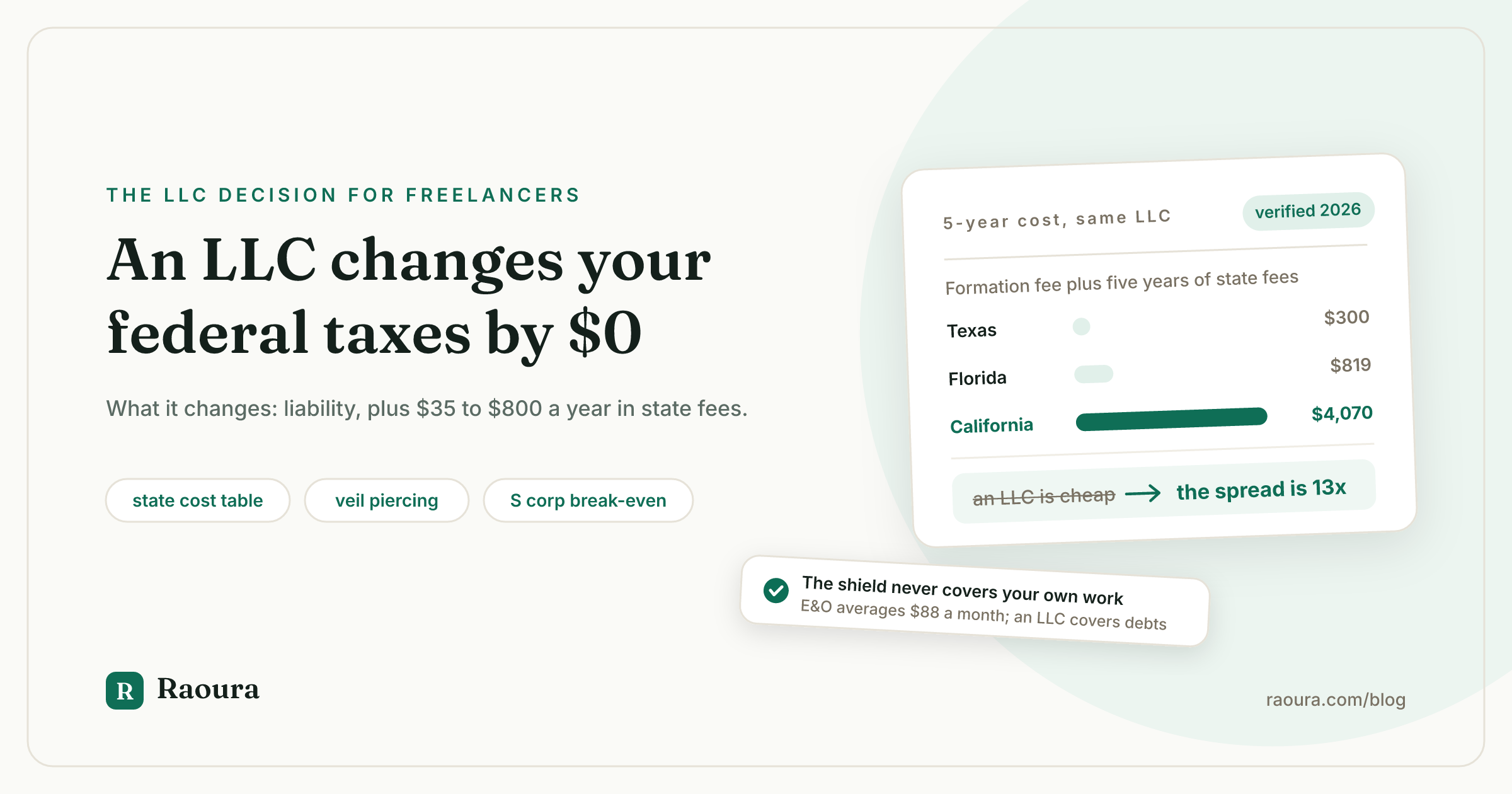

A single-member LLC changes your federal income tax by exactly $0; what it changes is liability protection, at a verified cost of $35 to $500 up front plus $0 to $800 per year depending on your state.

That one sentence resolves most of the anxiety. By default the IRS treats a single-member LLC as a disregarded entity: you file the same Schedule C, take the same deductions, and pay the same self-employment tax "in the same manner as a sole proprietorship," in the IRS's own words. The LLC is a legal container, not a tax strategy.

Which means the real question splits into three smaller, answerable ones:

- Is the liability protection worth the fees in your state? (Often yes, but it protects less than you think.)

- Would insurance cover your actual risk better or cheaper? (For pure professional mistakes, yes.)

- When does the tax math ever change? (Only when you layer an S corp election on top, and only above a certain profit level.)

The rest of this article takes those in order, with the state cost table most pages refuse to publish.

What each one actually is#

Roughly 86 percent of America's 29.8 million nonemployer businesses are sole proprietorships, which makes the default choice the overwhelmingly normal one.

A sole proprietorship is what you already are. Per the SBA, you are automatically a sole proprietor if you do business activity without registering as anything else. There is no formation paperwork and no federal filing. If you want to operate under a name other than your own ("Hazel Creative" instead of "Hazel Nguyen"), you register a DBA, a doing-business-as or fictitious name, with your state, county, or city. A DBA is a label, not a legal shield.

A limited liability company is a state-created legal entity that exists separately from you. You form one by filing articles of organization with your state (not articles of incorporation, whatever the top-ranking pages say) and paying a filing fee. The company, not you personally, then signs contracts, owes debts, and holds the business bank account.

For scale: the Census Bureau counts 29.8 million nonemployer businesses in the US, and its own methodology notes put sole proprietorships at about 86.4 percent of them. Most working freelancers never form an entity, and most of them are fine. That is not an argument against the LLC; it is an argument against forming one out of vague dread.

The tax myth, killed with IRS citations#

A sole proprietor and a single-member LLC with identical income pay identical federal tax: the same 15.3 percent self-employment tax, the same income tax brackets, and the same 20 percent QBI deduction.

This is the single most useful fact in the whole comparison, and the pages selling formation services have no incentive to lead with it. Point by point:

Self-employment tax is the same. SE tax runs 15.3 percent (12.4 percent Social Security plus 2.9 percent Medicare) on 92.35 percent of your net earnings, whether Schedule C says "sole proprietor" or "single-member LLC" at the top. The Social Security portion caps at the wage base, which is $184,500 for 2026; the Medicare portion never caps. On $60,000 of net profit, that is about $8,478 of SE tax either way.

The deductions are the same. A stubborn myth says an LLC "unlocks" business deductions. It does not. Home office, software, equipment, health insurance premiums, retirement contributions: every deduction available to a single-member LLC is equally available to a sole proprietor, because the IRS is looking at the same Schedule C. (One ranking page claims the opposite. It is wrong.)

The QBI deduction is the same. The 20 percent qualified business income deduction applies to both structures identically, and the 2025 tax law made it permanent: the OBBBA locked in the 20 percent rate, raised the phase-in ranges for the limitation thresholds, and added a minimum $400 deduction for anyone with at least $1,000 of qualified business income from an active business. None of the five top-ranking pages we checked mentions this 2026 status at all.

If you are still working out what all of this means for your set-aside rate, our breakdown of the 25 to 30 percent rule runs the full math at three income levels, and the quarterly estimated tax guide covers when the money actually goes out the door. Nothing in either article changes based on whether you form an LLC.

What an LLC actually protects (and what it never will)#

An LLC can shield your personal assets from business debts and contract claims, but it does not protect you from your own professional mistakes, which is the number one risk most freelancers actually face.

Here is the honest version of the liability story, which almost no ranking page tells straight.

What the shield covers: if the business owes money it cannot pay (a lease, a vendor bill, a business loan you did not personally guarantee) or gets sued over something the business did that you did not personally do, a properly maintained LLC keeps the claim against the company's assets, not your house and savings. For a freelancer who signs office leases, hires subcontractors, or carries business debt, that is real protection.

What it never covers: you. If a client sues you because your work was allegedly negligent, late, defective, or caused them losses, you performed that work personally, and personal liability for your own acts follows you through any entity. A web developer whose bug takes down a client's store, a consultant whose advice backfires: the LLC does not make that lawsuit go away. This is precisely what professional liability (errors and omissions) insurance exists for, and it is not expensive: Insureon's data across 100,000 small business policies puts the average at $88 per month (about $1,051 per year), with 43 percent of customers paying under $75 per month and lower-risk professions averaging around $42.

And the shield is conditional. Courts can pierce the veil and reach your personal assets when the entity is abused, and the textbook example Cornell's Legal Information Institute gives is intermingling personal and business assets. Run client payments into your personal checking account, pay your rent from the business account, skip the operating agreement, and you have spent hundreds of dollars a year on a shield a lawyer can fold in one deposition.

That last point has a practical corollary: the LLC is only as strong as your bookkeeping discipline. Separate bank account, contracts signed in the company name, invoices issued by the company, money flowing business-account-first, always. This is one of the quiet reasons we built Raoura the way we did (disclosure: Raoura is our product): your contracts, invoices, and payment records all live under your business name in one place, and payments run through your own Stripe account straight into your business bank account, so the paper trail that keeps a veil intact builds itself while you work. Any system that keeps business money and business documents cleanly separated does the job; the point is that "I'll clean it up later" is how shields fail.

What an LLC costs, state by state (verified July 2026)#

Formation filing fees run from $35 in Montana to $500 in Massachusetts, and the five-year cost of the same LLC is about $300 in Texas versus $4,070 in California, a difference of more than 13x.

This is the table the affiliate pages will not print, because "it depends on your state" keeps you clicking. Every figure below comes from the state's own filing office or tax agency, checked this month.

| State | Fee to form | Every year after | The catch |

|---|---|---|---|

| California | $70 | $800 minimum franchise tax | Due every year even at $0 income, until you formally cancel. Extra fee tiers start above $250,000 of CA income. The first-year waiver expired for LLCs formed after 2023. |

| Texas | $300 | $0 franchise tax below $2.65M revenue | A Public Information Report is still due annually even when no tax is owed. |

| New York | $200 | Biennial statement (small fee) | The publication requirement: notices in two newspapers for six consecutive weeks within 120 days, plus a $50 certificate. Newspaper rates commonly total an estimated $300 to $1,200+, highest in Manhattan. Skip it and your authority to do business is suspended. |

| Florida | $125 | $138.75 annual report | File after May 1 and the late fee makes it $538.75. |

| Delaware | Standard filing fee applies | $300 flat annual tax | Due June 1, no report required; $200 penalty plus 1.5% monthly interest if late. A pending 2026 bill proposes raising it to $400. Almost never worth it for a solo who lives elsewhere (you would pay Delaware and register in your home state too). |

| Montana | $35 | Annual report required (small fee) | Cheapest verified formation fee in the country. |

| Massachusetts | $500 | Annual report required | Most expensive verified formation fee. |

Run the five-year math and the spread gets dramatic. A Texas freelancer under the revenue threshold pays $300 total. A Florida freelancer pays $818.75 ($125 plus five annual reports at $138.75). A California freelancer pays $4,070 ($70 plus five years of the $800 franchise tax), before a single hour of accounting help. Same legal structure, same protection, a 13x difference in carrying cost.

Two takeaways from the table. First, the decision genuinely is state-specific: "an LLC is cheap, just do it" is true in Montana and false in California. Second, form in the state where you live and work. The Wyoming-or-Delaware-LLC advice that circulates in freelancer forums generally backfires for solos, because your home state will require you to register the out-of-state LLC as a foreign entity anyway, and then you pay two states forever.

The S corp layer: when the tax math finally changes#

An S corp election starts saving a freelancer real money somewhere between $60,000 and $80,000 of net profit for most people, because the savings must outrun $1,500 to $3,000 per year of new payroll and tax-prep costs.

Everything above holds for a default LLC. The tax math only changes if your LLC files Form 2553 and elects S corporation treatment, which the IRS explicitly permits for qualifying LLCs.

The mechanism: as an S corp, you become your own W-2 employee. You must pay yourself a reasonable salary for the work you do, and that salary gets hit with the same 15.3 percent in payroll taxes that SE tax would have taken. The remaining profit comes out as a distribution that avoids the 15.3 percent entirely. The savings live in the gap between your profit and your salary.

Worked example at $80,000 of net profit. As a default LLC or sole proprietor, SE tax is 15.3 percent of 92.35 percent of $80,000, about $11,304. As an S corp paying a $50,000 salary, payroll taxes take 15.3 percent of $50,000, or $7,650, and the remaining $30,000 distribution escapes. Gross saving: about $3,650.

Now subtract what nobody advertises: an S corp files its own tax return (Form 1120-S), runs actual payroll with quarterly filings, and typically needs a payroll service and a preparer. Realistic added cost is $1,500 to $3,000 a year. Your $3,650 gross saving nets out somewhere between $650 and $2,150, and a too-low salary invites IRS scrutiny, because reasonable compensation is a requirement, not a suggestion. (The salary also reduces your QBI deduction base, which shaves the savings further; the clean version of that interaction is its own article.)

Where is the break-even? Here the sources honestly disagree, and you should know that they disagree: the most aggressive credible source, a CPA writing for Keeper, puts the start-thinking-about-it line around $30,000 of net income, while most CPA firms we surveyed this month cluster around $60,000 to $80,000 before the election clearly pays. Our own math above explains the gap: at $30,000 of profit the gross savings and the admin costs nearly cancel, so the answer depends entirely on how cheaply you can run payroll. Below roughly $50,000, skip it. Above $80,000, run the numbers with a CPA. In between, the deciding variable is admin cost, not tax rate.

One sequencing note: the S corp question is separate from the LLC question. You can form the LLC now for liability reasons and elect S corp status in a later year when the profit justifies it. You do not need to decide both today.

The decision, stated plainly#

Stay a sole proprietor if you are under about $50,000 of profit with low contract risk; form an LLC when clients, leases, or subcontractors enter the picture; add the S corp election only when profit clears the admin costs.

Choose to stay a sole proprietor for now if most of these are true: you are early or part-time, your clients are small and your projects low-stakes, your state makes LLCs expensive (California's $800 per year buys a lot of E&O insurance), and you carry professional liability insurance for the risk that actually worries you. You lose nothing by waiting; the entity can be formed in an afternoon whenever the picture changes.

Choose to form an LLC if any of these are true: you sign leases, take on business debt, or hire subcontractors; your projects are large enough that a contract dispute could be existential; clients or their procurement departments expect an entity (some enterprise clients simply pay LLCs faster and with fewer vendor-onboarding questions); or your state's carrying cost is trivial and you value the separation. Get the EIN (free, directly from the IRS, never from a paid intermediary), open the business bank account, write an operating agreement even though you are the only member, and route everything through the company from day one.

And in either structure, put your protection where the risk actually lives: a real contract on every project and insurance for your professional work. A solid freelance contract with a limitation-of-liability clause does more for most freelancers than any entity choice, and it costs nothing.

Frequently asked questions

Does an LLC lower a freelancer's taxes?

No. By default a single-member LLC is a disregarded entity: same Schedule C, same deductions, same 15.3 percent self-employment tax, same QBI deduction as a sole proprietor. Federal taxes change only if the LLC elects S corp (or C corp) treatment, and state fees like California's $800 annual franchise tax mean an LLC often raises your total tax cost.

Do I need an LLC to freelance legally?

No. You are automatically a sole proprietor the moment you do business, per the SBA, and about 86 percent of US nonemployer businesses run exactly that way. You may need local business licenses and a DBA for a trade name, but no entity is required to invoice clients legally.

Will an LLC protect me if a client sues over my work?

Mostly no, and this is the most dangerous myth in the comparison. You are always personally liable for your own professional acts, so a claim that your work was negligent or defective reaches you regardless of entity. That risk is what professional liability (E&O) insurance covers, at an average of about $1,051 per year per Insureon's policy data. The LLC shield covers business debts and obligations, not your own mistakes.

Can I start as a sole proprietor and form an LLC later?

Yes, and that is the standard path. The entity can be formed at any point, and by default nothing about your federal income taxes changes when you do. You will need a new EIN and bank account for the LLC, updated contracts and W-9s in the company name, and a clean cutover date. The mechanics deserve their own walkthrough.

Is a single-member LLC worth it in California?

The bar is higher than anywhere else: $800 per year in franchise tax, every year, even at zero income, until you formally cancel. That is roughly the cost of a year of professional liability insurance for a typical freelancer. Plenty of California freelancers still form LLCs for contract-heavy work, but "everyone should just get an LLC" advice written from a $35-Montana perspective does not survive contact with the FTB.

One standalone fact worth keeping: forming an LLC changes a solo freelancer's federal income tax bill by exactly zero dollars unless the LLC also files a corporate election. The IRS treats you as the same Schedule C business either way.

Every figure above was verified in July 2026 against irs.gov (single-member LLC, self-employment tax, Form 2553, and OBBBA provisions pages), ssa.gov (2026 wage base), state filing offices (California SOS and FTB, Texas SOS and Comptroller, New York DOS, Florida Sunbiz, Delaware Division of Corporations, Montana SOS, Massachusetts SOC), census.gov, Cornell Law's Legal Information Institute, and Insureon's published policy data. State fees change; check your state's filing office before you file. This is general information, not legal or tax advice.

Run your client work in one place

Send a proposal, get it signed, invoice, and get paid, with a branded portal your clients will actually use. One flat plan at $17/month, and we never take a cut of your payments.

Try Raoura free for 14 daysNo credit card required. Set up in minutes.

Keep reading

The Best Client Portal Software for Freelancers in 2026: 10 Tools Audited, No Vendor Spin

Every page ranking for this query is a vendor putting itself at #1, and three of them still recommend a product that changed its name ten months ago. We audited 10 client portals against the six things that matter for a business of one: verified pricing, portal tier gates, client caps, white label, login friction, and payment fees.

7 Bonsai Alternatives Now That Bonsai Belongs to Zoom (2026)

Zoom acquired Bonsai in late 2025, Bonsai's blog has been quiet since March 2025, and the product is drifting toward agencies. Here are 7 alternatives for solo freelancers, with verified pricing and the fee math Bonsai does not lead with.

7 Dubsado Alternatives That Do Not Need a $2,000 Setup Specialist (2026)

Dubsado's power comes with a catch: new pricing of $35 to $55 per month, and a setup so involved that certified specialists charge $2,000 to $3,500 to do it for you. Here are 7 alternatives you can set up in an afternoon.